Dispelling misconceptions about current state of the Chinese economy

Editor's Note:

"Cognitive Warfare" has become a new form of confrontation between states, and a new security threat. With new technological means, it sets agendas and spreads disinformation so as to change people's perceptions and thus alter their self-identity. Launching cognitive warfare against China is an important means for Western anti-China forces to attack and discredit the country. Under the manipulation of the US-led West, the "China threat theory" has continued to foment.

Some politicians and media outlets have publicly smeared China's image by propagating false narratives such as "China's economy collapse theory" and "China's virus threat theory," in an attempt to incite and provoke dissatisfaction with China among people in some countries. These means all serve the seemingly peaceful evolution strategy of the US to contain China's rise and maintain its hegemony.

The Global Times is publishing a series of articles to systematically reveal the intrigues of the US-led West's cognitive warfare targeting China, and expose its lies and vicious intentions, in an attempt to show international readers a true, multi-dimensional and panoramic view of China.

This is the third installment in the series.

In the ongoing process of China's post-pandemic economic recovery, much like many other nations, the world's second-largest economy is faced with its share of challenges with ups and downs more frequently seen in its capital market in recent months.

Yet, some Western media outlets have seized on this as an opportunity to create a series of narratives that could discredit the nation. These narratives included but are not limited to claims of Chinese residents becoming "too fearful to spend," assertions that China is hemorrhaging foreign capital, proclamations of China descent into deflation, and, some claims that Chinese policymakers are unable to find a solution.

Even US President Joe Biden has added fuel to the flames, calling China's economy a "ticking time bomb" and warned that "China is in trouble."

These ostensibly reasonable yet factually unsubstantiated statements, skillfully packaged and disseminated by some mainstream media outlets, have continued to brew, depicting a China that appears vulnerable and teetering on the brink of collapse according to the global perception.

Many narratives have prevailed until now - even though a slew of economic indicators already show that China has once again defied expectations, breaking through the waves of uncertainty with its monthslong stimulus and manufacturing strength - resulting in pessimism about China's economic prospects bolstered by numerous misconceptions.

It's therefore necessary to list some prevailing, typical lies and misconceptions surrounding the world's second-largest economy, make clarifications, and present a factual and data-driven portrayal of China's economic realities.

Misconception 1: Deflation economy

One of the most widespread claims is that Chinese residents are becoming more reluctant and "too fearful to spend," which results in deflation.

Stories such as "Households would rather save than spend" or "China's shoppers hesitate to spend in face of deflation" have become commonplace in some highly-regarded Western media outlets since from the beginning of the year. A New York Times report published in August painted a more pessimistic picture, saying that Chinese consumers and business owners "feel paralyzed by despair," and their reluctance to spend and borrow is feeding what could become "a dangerous cycle."

But the truth is, as residents' income has stabilized after the pandemic, and offline consumption scenarios recover, so too is there a gradual increase in Chinese people's willingness to consume.

To measure residents' consumption inclination, one can look at the ratio of household consumption expenditure to disposable income. In the second quarter, this indicator had already rebounded to 68 percent, narrowing the gap with the pre-pandemic period (2015-2019) from 4.5 percentage points in the first quarter to 2.8 percentage points, according to a research report by TF Securities.

A slew of data also proved that residents' willingness to travel and spend continued to improve in the fourth quarter, largely unleashed by the eight-day long "Super Golden Week" in October. The country's domestic tourism market generated approximately 753.4 billion yuan ($103.2 billion) in revenue amid the holidays, representing a year-on-year increase of 129.5 percent and a rise of 1.5 percent from that of the National Day holidays in 2019, according to the Ministry of Culture and Tourism.

China's e-commerce platforms, which have kicked off the "Double 11" shopping festival this week, one of the country's most important online retail shopping events, also reported notable increases in sales. Data from Chinese e-commerce giant JD.com showed that on its first day of this year's "Double 11" shopping window, the number of users and transactions both quadrupled year-on-year in the first 10 minutes as the platform kicked off the promotion event at 8 pm Monday.

The hype over "China deflation" has been at its highest while China's consumer index remains low, but it has to be pointed out that deflation is an economic phenomenon that refers to a continuous decrease in the price of goods and services in an economy. China's consumer price index returning to positive territory in August effectively debunks the deflation fallacy, Cong Yi, a professor at the Tianjin University of Finance and Economics, told the Global Times.

In the first three quarters of this year, China's total retail sales of consumer goods increased by 6.8 percent year-on-year, showing an all-round rebound, with retail sales in the service sector, including transportation, accommodation, and catering experiencing a year-on-year growth of 18.9 percent.

"Drawing conclusions about deflation in the Chinese economy based on isolated data is purely motivated by ulterior motives - to peddle fear and anxiety, and frighten away global investors," Cong said.

Misconception 2: Manufacturing industry exodus, export engine failure

Reports that China is "uninvestable" and of "foreign capital flight" out of the country might be familiar to mainstream media readers. While such narratives are seemingly credible, and bolstered by US-led sanctions and crackdowns on Chinese firms and industries, there have been growing claims that this could lead to Chinese manufacturers being compelled to relocate or lose buyers, resulting in a continuous decline in export share and loss of competence in the nation's manufacturing strength.

However, the truth is capitals are clever and will only identify destinations where there are opportunities and profits to be made. As China's economy continues to enjoy robust development, creating broad demand across various sectors, and serving as a crucial engine for economic growth, China remains one of the most attractive investment destinations worldwide.

On one hand, the overall trend of increased foreign investment in China remains unchanged. According to the United Nations Conference on Trade and Development's "World Investment Report 2023," China continues to be the second-largest recipient of foreign direct investment globally.

Chinese Ministry of Commerce data shows that from January to August this year, there were 33,000 new foreign-funded enterprises established in China, representing a 33 percent year-on-year increase. European countries have significantly increased their investments in China, with actual investment from the UK, France, Switzerland, the Netherlands, and Germany growing by 132.6 percent, 105.6 percent, 59.2 percent, 25.3 percent, and 20.8 percent respectively.

Executives from multinational corporations like Tesla, Apple, and Nestlé have visited China since pandemic restrictions were lifted, demonstrating their trust in China as an investment destination.

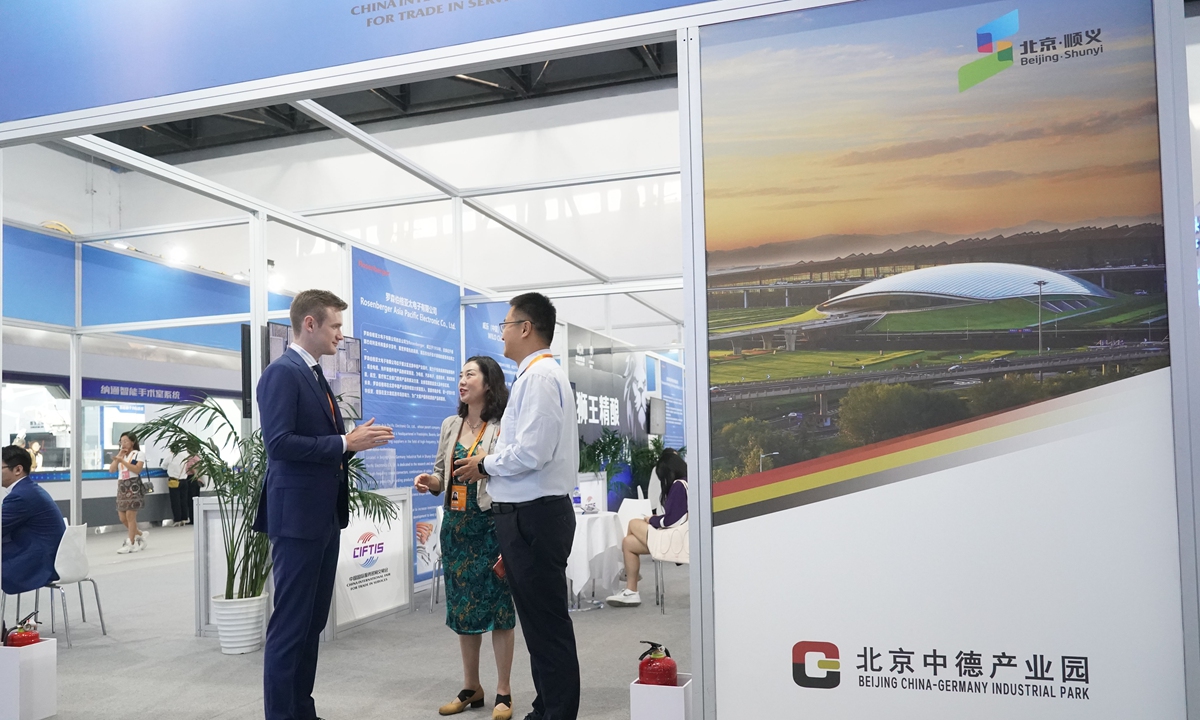

Participants at an exhibition booth of the Beijing China-Germany Industrial Park in the China National Convention Center, during the 2023 China International Fair for Trade in Services, on September 4, 2023. Photo: Xinhua

On the other hand, China's industrial upgrading efforts have been steadily bearing fruit, with high-tech industries becoming a hotbed of foreign investment. China is deeply integrated into the global value chain, and the proportion of high value-added products in imports and exports continues to rise. Exports of "new three" products, including lithium batteries, electric vehicles, and solar panels, have maintained double-digit growth for 14 consecutive quarters.

Moreover, exporters told the Global Times that amid China's industrial upgrading and greater push for de-carbonization, relocation of factories, mainly centered on labor-intensive industries to other parts of the world, are happening. But what was lost in terms of consumer goods exports due to companies moving abroad was compensated by an increase in exports of intermediate and capital goods.

Companies expanding overseas for production may benefit from advantages related to labor, raw materials, tariffs, logistics, legal considerations, and more. However, during the investment phase, they often need to import capital goods, and in the production phase, they rely on importing intermediate goods, which are mainly from China, they said.

One closely watched set of data is China's trade figures for September, which registered month-on-month growth for a second consecutive month, with the trade volume reaching a new monthly high for the year, hitting 3.74 trillion yuan, data from the General Administration of Customs showed.

Zhou Maohua, an economist at the China Everbright Bank, said that September data shows "remarkable stability" in Chinese trade as it was achieved amid a challenging global demand environment, and substantial declines in exports from some of China's major trading partners.

"With strong policy support, concerted efforts from businesses, and collaboration from all sides, the export trend in the fourth quarter is expected to continue stabilizing and improving," Lü Daliang, spokesperson from the General Administration of Customs, told a press conference in Beijing last week.

Misconception 3: Running out policy tools

Notably, every time the Chinese economy stumbles or faces challenges, there is a tendency for some naysayers in the US media to say that finally the end is near, believing that policymakers are running out of tricks to "save the economy from impending disaster."

The "China collapse" theory has become more persuasive amid challenges seen in China's real estate sector, with financial woes affecting a couple of debt-ridden developers like Evergrande. But the impact of real estate, it though accounts for a significant portion of residents' assets, might be exaggerated.

Real estate woes will become dangerous when borrowers default on their mortgages, as happened in the US during the financial crisis of 2008, causing shockwaves across the whole board. But in China, it is a very different story.

Between 2018 and 2019, which marked a period of high mortgage interest rates, over 90 percent of homebuyers had down payment ratios of 30 percent or more, indicating a low possibility of default, according to the TF Securities report, citing data from sample banks regarding the down payment ratios for first-time homebuyers.

Therefore, despite a slight decline in property prices from their peak during these years, real estate did not become a "negative asset." Instead, residents chose to repay their mortgages in advance rather than defaulting on them, the report explained.

In addition, the scale of real estate-related financial derivatives in China is relatively small.

Many also suggest that the Chinese economy resembles Japan's economy of the past and may face long-term recession as a form of comparison. They however neglect certain obvious facts including China has its advantage of policy independence, a vast domestic market, and ample policy reserves.

Since August this year, the Chinese government has increased the implementation of macro policies related to finance and currency. It has continued to optimize tax incentives and introduced a range of practical new measures to support the real economy and private enterprises.

The effectiveness of the current policy mix is already evident. Official data released last week showed China's third-quarter growth came in much stronger than expected, boosting hopes that the world's second-largest economy is almost certain to exceed the yearly growth target of around 5 percent in 2023.

In another move which underscores Chinese policymakers' resolve and ability to navigate serious downward pressures, on Tuesday, the sixth session of the Standing Committee of the 14th National People's Congress approved the issuance of an additional 1 trillion yuan in special treasury bonds.

The plan evidently helped boost market expectations as major Chinese stock indexes made gains on Wednesday.

"China is projected to grow 5 percent this year. As a result, it will contribute roughly one-third of total global GDP growth," Steven Barnett, IMF Senior Representative for China, said at the launch of the IMF World Economic Outlook 2023 in Beijing earlier this month.

This may to the disappointment of those who hyped over "China collapse" story, as China, who has been the global growth driver with astonishing growth speed in recent decades, will likely continue to lead the way ahead this year though challenges are mounting.

Photos

Related Stories

- China increases digital trade in its opening-up endeavors

- Interview: Economist predicts supportive measures will lead to Chinese economy bottoming out

- Interview: China's economy enjoys strong flexibility, resilience, says Egyptian expert

- China's financial system pledges efforts to serve real economy

- China's central bank adds liquidity via reverse repos

- Interview: Higher-than-expected growth points to resilience of Chinese economy, says economist

- Interview: Economist says China has ample policy space to boost economy

- Commentary: China's economy disappoints naysayers again

- Commentary: China's pro-growth measures boost economic recovery, confidence

- Q3 data reveals China's economic recovery gathering steam

Copyright © 2023 People's Daily Online. All Rights Reserved.